CoinJar Taxes: How to Generate Your Crypto Tax Report

CoinJar does not create a tax report for you. Every crypto trade and disposal is a potential tax event you are responsible for declaring. CoinTracking imports your full CoinJar transaction history via CSV export, calculates gains and losses, and generates a tax report ready for your tax authority or accountant.

How to Import Your CoinJar Transactions into CoinTracking

Watch how to export your transaction history from CoinJar as a CSV file and import it into CoinTracking to generate your crypto tax report.

Start Your Free CoinJar Import- Every crypto trade on CoinJar is a taxable disposal in most jurisdictions. Capital gains tax applies when you sell, swap or spend crypto.

- CoinJar supports CSV export for tax reporting. Download your transaction history from your CoinJar account and upload it to CoinTracking for automatic import and tax calculation.

- Transfers between your own wallets are not taxable events. Buying and holding crypto is not a taxable event.

- CoinJar is an Australian exchange with UK FCA registration — it is not EU-regulated and not subject to DAC8. However, you are still legally required to self-report all crypto gains to your tax authority. Tax enforcement around crypto is growing globally, and undisclosed gains carry increasing risk of penalties.

CoinJar and Your Tax Obligations

CoinJar is an Australian crypto exchange founded in Melbourne in 2013. It holds an Australian Financial Services Licence (AFSL) and is registered with the UK Financial Conduct Authority (FCA), making it one of the few exchanges with dual Australian-UK regulatory standing. CoinJar is not an EU-regulated entity and does not fall under DAC8 reporting obligations.

CoinJar does not automatically generate tax reports or report your transactions to tax authorities. All self-reporting obligations remain with you. CoinTracking imports your CoinJar data via CSV and automates the entire calculation process.

CoinTracking supports CoinJar via CSV file upload:

- CoinJar CSV export: downloaded from your CoinJar account transaction history or statements section

- All crypto buy, sell, and swap transactions are supported

- CoinTracking maps CoinJar CSV columns automatically

- Compatible with all CoinJar products including CoinJar Exchange

Crypto Tax Basics: What CoinJar Users Need to Know

Tax rules for crypto vary across jurisdictions. These principles apply broadly to CoinJar users, but always verify the specifics with your local tax authority or a qualified advisor.

Trading crypto is a taxable disposal

In most countries, every sale, swap or use of crypto is a taxable event. Capital gains tax applies to the difference between what you paid (cost basis) and what you received. Transfers between your own wallets do not trigger tax.

CoinJar does not report to your tax authority — but you must

CoinJar is an Australian-based exchange registered with the UK FCA. It is not subject to EU DAC8 reporting obligations. However, this does not reduce your personal tax obligations. Tax authorities worldwide are increasing crypto monitoring through on-chain analysis, exchange data requests, and international information-sharing agreements. Self-reporting remains your legal duty.

Records are your responsibility

CoinJar does not issue formal tax documents. The CSV export is a raw transaction history — not a tax report. Accurate records of every trade, date, cost and proceeds remain your responsibility. CoinTracking maintains a complete, dated audit trail of every CoinJar transaction you import.

CoinJar Taxes by Country

Crypto tax rules differ by market. Below are the key rates, deadlines and filing forms for the countries where CoinTracking users trade most actively on CoinJar.

Germany

Germany

- Disposal tax: Personal income tax rate (up to 45%); gains are tax-free if held longer than 1 year (Haltefrist)

- Annual exemption: Gains up to €1,000/year are tax-free

- Staking income: Taxed as other income (Sonstige Einkünfte)

- Cost basis: FIFO per wallet

- Authority: Finanzamt

- Forms: Anlage SO, Anlage KAP

Austria

Austria

- 27.5% capital gains tax: Since March 2022, crypto is taxed like shares — a flat 27.5% KESt applies to gains.

- Old coins grandfathered: Crypto acquired before 28 February 2021 is tax-free on disposal.

- Staking and lending: Treated as capital income, also taxed at 27.5%.

- Authority: Finanzamt Austria. Report via Einkommensteuererklärung (E1 / E1kv).

Switzerland

Switzerland

- Capital gains: Generally tax-free for private investors (no capital gains tax on crypto disposals for non-professionals)

- Wealth tax: Crypto holdings are subject to wealth tax at cantonal rates based on year-end market value

- Income from crypto: Mining and staking rewards are taxed as income at progressive rates

- Authority: Cantonal tax authority (varies by canton)

United Kingdom

United Kingdom

- Capital Gains Tax: 18% (basic rate) or 24% (higher rate) from October 2024

- Annual exempt amount: £3,000 (2024/25 onward)

- Staking income: Income Tax at marginal rate

- Cost basis: Section 104 pool (HMRC rules)

- Authority: HMRC

- Forms: Self Assessment SA100, SA108

- Note: CoinJar is FCA-registered in the UK. UK is post-Brexit and not subject to EU DAC8 reporting. You must self-report via Self Assessment.

Spain

Spain

- Savings income (IRPF): 19% up to €6,000; 21% up to €50,000; 23% up to €200,000; 27% up to €300,000; 28% above

- Foreign crypto disclosure: Modelo 721 required if portfolio exceeds €50,000 abroad

- Staking income: Taxed as savings income

- Authority: Agencia Tributaria (AEAT)

- Forms: Modelo 100 (IRPF), Modelo 721

Poland

Poland

- Flat rate: 19% on all crypto gains (no holding period exemption)

- Loss carryforward: Up to 5 years

- Staking income: Taxed as capital income at 19%

- Cost basis: FIFO

- Authority: Urząd Skarbowy

- Form: PIT-38

Italy

Italy

- Flat rate: 26% on gains exceeding €2,000/year (from 2023)

- Foreign holdings disclosure: Quadro RW required if portfolio exceeds €15,000

- Staking income: Taxed as capital income at 26%

- Authority: Agenzia delle Entrate

- Forms: Quadro RT (gains), Quadro RW (foreign holdings)

Portugal

Portugal

- Disposal tax: 28% on gains from crypto held less than 1 year (from 2023)

- Long-term holding: Tax-free on disposal if held 1 year or longer

- Staking income: Taxed at 35% flat rate or progressive income tax rates

- Authority: Autoridade Tributária (AT)

- Forms: Modelo 3, Anexo G or Anexo J

France

France

- Flat 30% tax (PFU): Gains from crypto disposals are subject to the prélèvement forfaitaire unique (PFU) — 12.8% income tax + 17.2% social charges.

- No exemption for holding period: Unlike Germany, there is no tax-free threshold after 1 year.

- Staking income: Taxed as BNC (non-commercial income) if received regularly; otherwise as capital gains.

- Authority: Direction générale des Finances publiques (DGFiP). Declare via Formulaire 2086.

Australia

Australia

- Capital Gains Tax (CGT): Crypto is treated as a capital asset. Gains are included in assessable income and taxed at your marginal income tax rate.

- 50% CGT discount: If you hold a crypto asset for more than 12 months before disposing of it, you may be eligible for a 50% CGT discount (for individuals).

- Staking and DeFi income: Treated as ordinary income at the time of receipt, taxed at your marginal rate.

- ATO reporting: The Australian Taxation Office (ATO) actively monitors crypto transactions. All gains must be reported in your annual tax return.

- Authority: Australian Taxation Office (ATO)

- Forms: Annual Income Tax Return (myTax or paper return, Capital Gains schedule)

Tax rules change frequently. This overview is for general information only and does not constitute tax advice. Consult a qualified advisor for your specific situation.

Are CoinJar Transactions Taxable?

In most jurisdictions, crypto is treated as an asset: disposing of it can trigger capital gains tax. Use this as a starting reference. The exact rules vary by country.

Taxable Events

- Selling crypto for fiat (EUR, USD, AUD, GBP, etc.)

- Swapping crypto for crypto

- Using crypto to pay for goods or services

- Receiving crypto as income or reward

Not Taxable

- Buying and holding crypto

- Transferring crypto between your own wallets

- Depositing fiat to CoinJar

- Receiving crypto as a personal gift

Tax treatment varies by country. CoinTracking applies the rules for your selected jurisdiction automatically.

How to Calculate Your CoinJar Taxes

CoinJar's CSV export contains your raw trade history — but converting that into an accurate tax report requires calculating cost basis, holding periods and gains for every transaction.

The core calculation is straightforward: take what you received (proceeds), subtract what you paid (cost basis), and the result is your taxable gain or loss. For Australian users, the 12-month CGT discount eligibility must also be tracked for each individual lot. For UK users, HMRC's Section 104 pooling rules apply.

CoinTracking automates this across your full CoinJar history and produces a report your accountant or local tax authority will accept.

How to Import CoinJar into CoinTracking

Three steps to upload your CoinJar transaction history and generate your tax report.

- 1

Log into CoinTracking and open Imports

After logging in, click the Import icon in the left navigation. This is where you connect all your exchanges, wallets and blockchains.

- 2

Search for CoinJar in the import list

Type "CoinJar" in the search field. CoinTracking will show the CoinJar import option for CSV upload.

- 3

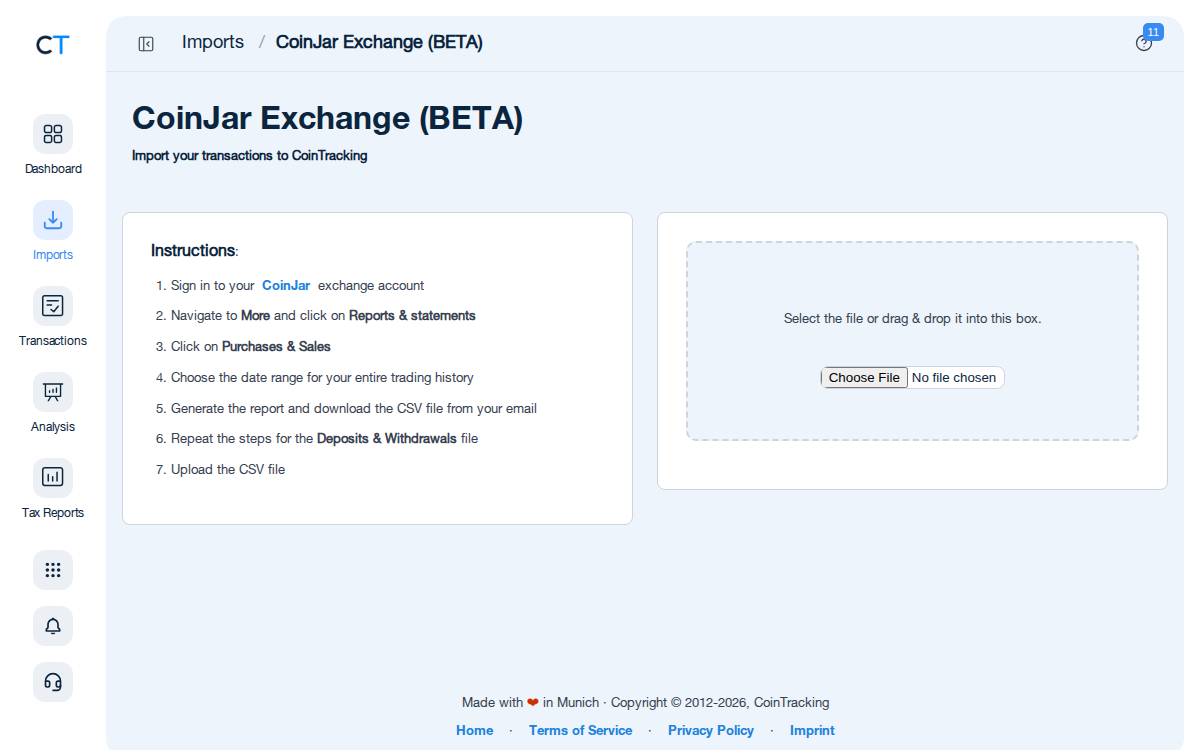

Upload your CoinJar transaction history

Log into CoinJar, export your transaction history as a CSV file, and upload it to CoinTracking. CoinTracking automatically maps CoinJar CSV columns and calculates your taxes.

"CoinTracking can handle just about any complex transaction you can throw at it and the automation is a real lifesaver. Of all the tax software tools we've reviewed, CoinTracking is the most detail-oriented and has more accuracy checks in place than the competition."

How to Create Your CoinJar

Tax Report with CoinTracking

Three steps from CSV export to a tax report your accountant will accept.

Export your CoinJar transaction history

Log into CoinJar, navigate to your account settings or statements section, and download your full transaction history as a CSV file.

Review your transactions

Open Reports → Validate Transactions. CoinTracking flags missing cost basis entries, duplicate imports and price gaps so your final report is accurate.

Generate and export your tax report

Select your country and tax year. CoinTracking generates a report formatted for your jurisdiction: PDF or Excel, ready to file or hand to your accountant.

No. CoinJar does not generate a tax report for users. It provides a transaction history export in CSV format from your account settings. You are responsible for converting that data into a jurisdiction-specific tax report. CoinTracking imports your CoinJar CSV and generates a complete, compliant report for your country.

Log into your CoinJar account, navigate to your account settings, find the transaction history or statements section, and download your transactions as a CSV file. Then upload the CSV file directly into CoinTracking to generate your tax report.

CoinJar is an Australian crypto exchange headquartered in Melbourne. It holds an Australian Financial Services Licence (AFSL) and is also registered with the UK's Financial Conduct Authority (FCA). CoinJar is not an EU-regulated entity and is not subject to DAC8 reporting obligations. However, regardless of exchange regulation, you are personally responsible for reporting all crypto gains to your local tax authority.

CoinJar primarily supports tax software integration via CSV export. Download your transaction history from your CoinJar account and upload it to CoinTracking. CoinTracking fully supports the CoinJar CSV format for automatic import.

In most countries, yes. Every sale, swap, or disposal of cryptocurrency is a taxable event. The gain or loss is the difference between your cost basis and the proceeds at the time of disposal. Tax-free thresholds and holding periods vary by jurisdiction: Germany offers a 1-year exemption, the UK has an annual CGT allowance, and Australia taxes crypto as a capital asset with a 50% CGT discount for assets held over 12 months.

Yes. Your tax obligations are independent of whether an exchange reports to your government. You are legally required to self-report all crypto gains and income in your tax return, regardless of which exchange you use or where it is based. Tax authorities in most countries have expanded crypto monitoring and enforcement — failing to declare is increasingly risky.

Start Tracking Your Crypto Taxes Today

Experience why 2.2 million users trust CoinTracking — sign up today for a seven-day free trial!