Tax authorities in the UK are paying closer attention to cryptocurrencies than ever. Whether you're trading Bitcoin, earning staking rewards, or experimenting with DeFi, your crypto activities may trigger tax obligations. And if you're considering not reporting those gains to HMRC, it's important to understand the consequences.

HMRC has significantly increased efforts to identify unreported crypto income. From data-sharing agreements with major exchanges to targeted investigations, the tools at their disposal are growing rapidly. Failing to report your crypto correctly could lead to hefty fines, back taxes, or even criminal prosecution in severe cases.

New to UK crypto tax rules? Check out our comprehensive Guide on Crypto Taxes in the UK.

Key Takeaways for Crypto Tax Reporting in the UK

- Crypto is taxable: HMRC treats most crypto transactions as subject to Capital Gains Tax (CGT) or Income Tax, depending on the nature of the activity.

- No reporting: Failing to report crypto gains or income can result in significant financial penalties, interest charges, or even criminal investigations.

- HMRC is watching: Through data-sharing agreements with exchanges and blockchain analysis, HMRC can trace your crypto activities.

- Record keeping is essential: Accurate records of transactions, costs, and dates are your best protection against disputes or audits.

- Voluntary disclosure helps: Coming forward before HMRC contacts you can significantly reduce penalties – or help you avoid them altogether.

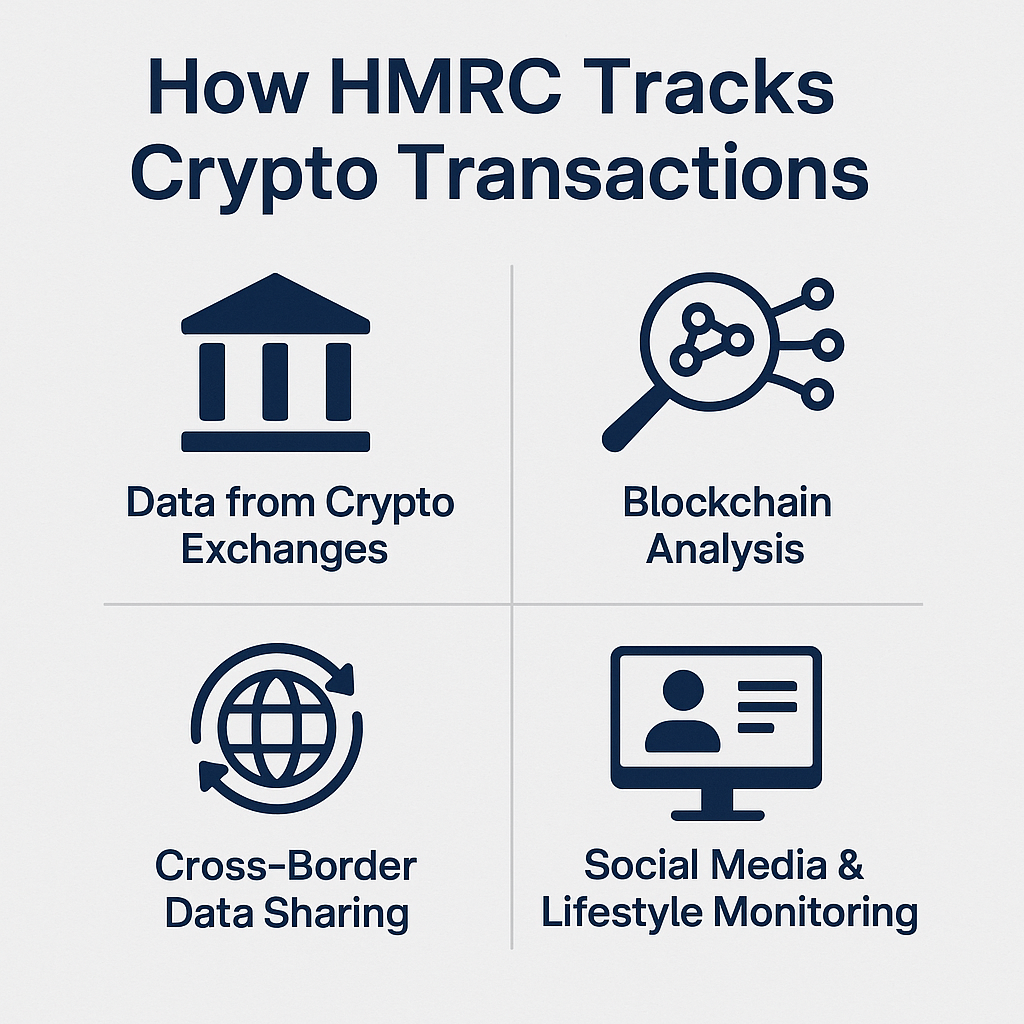

How HMRC Tracks Crypto Transactions

Many crypto users mistakenly believe that digital assets are anonymous – but that’s far from the truth. HMRC has developed several strategies to identify individuals who may owe tax on crypto transactions.

1. Data from Crypto Exchanges

HMRC has formal information-sharing agreements with major crypto exchanges like Coinbase, Binance, Kraken, and others operating in or serving UK customers. These platforms may be required to submit user data, including:

- Names and email addresses

- Transaction histories

- Wallet addresses

- Fiat on- and off-ramps

If you've used any major exchange, HMRC likely has visibility into at least part of your activity.

Transparency matters: Some exchanges, such as Coinbase and Kraken, regularly publish transparency reports in which they disclose how many requests have been received from investigative authorities and how often data has actually been released. These reports show how close the cooperation between crypto platforms and state authorities has become.

2. Blockchain Analysis

HMRC uses blockchain analytics tools to trace wallet addresses and follow the flow of funds. While pseudonymous, most blockchain transactions are fully transparent – and once a wallet is linked to an individual, all related transactions can be examined.

3. Cross-Border Data Sharing

Under the Common Reporting Standard (CRS), HMRC cooperates with tax authorities in other countries to share financial information. That means offshore exchanges and wallets aren’t a safe haven for avoiding tax obligations.

4. Social Media & Lifestyle Monitoring

HMRC increasingly monitors social media platforms, forums, and public posts to detect discrepancies between declared income and apparent wealth. Flashy crypto wins, luxury purchases, or NFT bragging can all raise red flags if they’re not reflected in your tax filings.

Think your crypto is invisible to HMRC? Think again. Digital footprints are traceable – even across multiple wallets, platforms, and social profiles.

Crypto Tax Deadlines & Penalties: What HMRC Does If You Miss the Report

If you fail to report your crypto gains or income on time, HMRC doesn’t just let it slide. There are clear deadlines for submitting tax returns and paying what you owe. Missing them can lead to financial and legal consequences.

HMRC Penalties for Unreported Crypto Gains

Once HMRC identifies a reporting failure, they may impose penalties based on how late the disclosure is and whether it was deliberate.

Financial Penalties

- Late filing penalties: £100 automatic fine if you miss the 31 January Self Assessment deadline.

- Inaccurate returns: If HMRC believes you submitted an incorrect return, penalties can range from 0% to 100% of the tax owed – depending on whether the mistake was careless, deliberate, or deliberate and concealed.

- Late payment interest: Interest accrues daily on unpaid taxes from the due date until payment is made.

Criminal Penalties

In rare but serious cases, especially where large amounts are involved or there’s evidence of deliberate tax evasion, HMRC may pursue criminal prosecution. This can result in:

- Court proceedings

- Asset seizures

- In extreme cases, imprisonment

Don’t ignore HMRC letters: If you receive a “nudge” letter or inquiry about crypto, respond promptly and seek professional advice. The CoinTracking Full-Service team reviews all your transactions, identifies reporting issues, and helps you generate accurate HMRC-compliant tax reports.

Missed the HMRC Crypto Deadline? Valid Excuses Explained

HMRC recognises that sometimes there are legitimate reasons for missing a tax deadline. While not all excuses are accepted, providing a reasonable explanation can help you avoid or reduce penalties.

Acceptable “Reasonable Excuses” (official HMRC criteria)

- Serious or unexpected illness (your own or a close relative's), including hospital stays

- Bereavement of a partner or close family member near the tax deadline

- Computer or software failure, including HMRC system outages during filing

- Fire, flood, theft that prevented you from completing your tax return

- Postal delays, if submitted by post on time

- Disability, serious mental health issues, or unexpected events affecting ability to file

- Misunderstanding or unawareness of the obligation – rarely accepted, but possible

- Reliance on another person, like an agent, that failed – if you took reasonable care

Important: Simply forgetting or being unaware of the rules is not considered a valid excuse. Lack of knowledge about crypto tax obligations won’t exempt you from penalties. Read our UK Crypto Tax Guide and make sure you're fully informed.

Your Crypto Portfolio Manager

What Does Not Count as a Reasonable Excuse

- Lack of funds or inability to pay

- Forgetting deadlines or not receiving reminders

- System complexity or confusion

- Relying on memory or third-party reminders not backed by reasonable care

- You made a mistake on your tax return

How to Fix Crypto Tax Mistakes Before It's Too Late

If you've made an error in your crypto tax reporting or failed to report at all – it’s not too late to act. HMRC allows taxpayers to correct mistakes voluntarily, and doing so promptly can significantly reduce penalties or even avoid them altogether.

1. Disclose Voluntarily

If you realise you've omitted or underreported crypto gains or income, you can make a voluntary disclosure through HMRC’s Digital Disclosure Service (DDS). This is the preferred route for:

- Missed crypto gains

- Misclassified income (e.g., staking or airdrops)

- Incomplete or inaccurate submissions

2. Amend a Tax Return

If your mistake was made in the most recent tax return (within 12 months of the filing deadline), you can usually amend it online via your HMRC account. This is faster and simpler than filing a full disclosure.

3. Seek Expert Help

Correcting crypto tax issues can be complex, especially if you’ve traded across multiple wallets, platforms, or blockchains. Using crypto tax calculators like CoinTracking helps you:

- Automatically import all transaction data – from buy and sell events to complex DeFi activities like staking, lending, and yield farming

- Reconstruct your entire transaction history

- Calculate gains using UK-compliant cost basis methods

- Prepare corrected tax reports

Need full support? The CoinTracking Full-Service team will review all your data, spot inconsistencies, and help you respond to HMRC properly.

Need clarity on DeFi taxes? Check out our guides on Crypto Staking Taxes in the UK and Crypto Lending Taxes in the UK.

Creating a Crypto Tax Return Made Easy

FAQ: What Happens If I Don't Report Crypto to HMRC

What should I do if I’ve missed reporting crypto?

Don’t wait for HMRC to contact you. Use their Digital Disclosure Service to voluntarily disclose any unpaid crypto tax. This can significantly reduce penalties and interest or even completely avoid them.

What are the reporting requirements for crypto gains in the UK?

You must report capital gains or income earned from crypto if your gains exceed the annual allowance. Activities that trigger tax include but are not limited to: Selling crypto for fiat, swapping one crypto for another, spending crypto on goods/services, earning crypto from staking, lending, airdrops, mining.

How can I keep accurate records of my crypto transactions?

You should log: Date and type of each transaction, asset type and amount, value in GBP, costs and fees, gains and losses, and counterparty (where applicable). CoinTracking helps automate this process with direct exchange/API imports and wallet tracking.

What are the penalties for late crypto tax reporting?

Penalties vary depending on the nature of the error and how quickly it’s corrected. You may face: £100 late filing fees, daily interest on unpaid tax, up to 100% (or 200% for offshore concealment) penalties for deliberate errors. See the full penalty table in the earlier section.

Is it possible to go to jail for tax evasion?

Yes, in rare but serious cases involving large sums or clear intent to defraud HMRC, criminal prosecution and imprisonment are possible. However, voluntary disclosure and cooperation can usually prevent this outcome.

Will HMRC Know If I Don’t Report My Crypto?

Very likely. HMRC obtains data from major exchanges, blockchain analytics tools, international partners, and even social media. Ignoring your reporting obligations is a high-risk move and illegal.

Conclusion - Avoid Crypto Tax Penalties by Reporting to HMRC

Ignoring your crypto tax obligations in the UK is not worth the risk. HMRC has multiple tools to detect unreported gains and income. If you’ve missed a deadline or made a mistake, taking proactive steps can help you avoid or minimize penalties. By using CoinTracking, you can simplify the process of tracking, calculating, and reporting your crypto transactions. And if things are already messy, the CoinTracking Full-Service team can help clean it up and get you back on track with HMRC.

Disclaimer

The information provided in this article is for educational and informational purposes only. It is not intended as financial, investment, tax, or legal advice. Cryptocurrency investments are highly volatile and carry significant risks. Before investing in cryptocurrencies, conduct thorough research, consult with a financial advisor, and ensure you understand the risks involved. The author and publisher are not responsible for any financial losses or damages that may occur from following the information presented in this article. Always use caution and make informed decisions when dealing with cryptocurrencies.